By Chris at www.CapitalistExploits.at

Market dislocations occur when financial markets, operating under stressful conditions, experience large widespread asset mispricing.

Welcome to this week's edition of “World Out Of Whack” where every Wednesday we take time out of our day to laugh, poke fun at and present to you absurdity in global financial markets in all its glorious insanity.

While we enjoy a good laugh, the truth is that the first step to protecting ourselves from losses is to protect ourselves from ignorance. Think of the "World Out Of Whack" as your double thick armour plated side impact protection system in a financial world littered with drunk drivers.

Selfishly we also know that the biggest (and often the fastest) returns come from asymmetric market moves. But, in order to identify these moves we must first identify where they live.

Occasionally we find opportunities where we can buy (or sell) assets for mere cents on the dollar - because, after all, we are capitalists.

In this week's edition of the WOW we're covering the death of active investing (or not)

Scan the financial news today and amongst the rubble 3 things stand out.

- US politics is now officially at the top of the fruit-bowl after entering banana republic territory.

- Sadly what happens to Kim Kardashian, who as far as I can tell is famous for being famous, is more important than wealth inequality, the demographic timebomb, unfunded pensions, and (amazingly) the headache I got after seeing her on Bloomberg. Yes, really.

- Active investing will blow away in the winds of history, replaced by passive strategies. Yup, it's over, folks. Thanks for playing.

It is the 3rd point that we lend our eye to here today.

But first let me state my bias up front. It's important for you to know so you can critique objectively - something we should all do.

Many many of my friends and colleagues manage money (some of them godawful amounts of the stuff), and many of them have been facing redemptions over the past few years with this year 2016 being the worst yet.

The WSJ recently ran an article about the dying business of picking stocks:

A few months ago Perry Capital closed its doors after losing over half of its capital to redemptions. As reported by Bloomberg:

"The closure is the latest -- and almost certainly not the last -- in what is shaping up to be the biggest shakeout in the $2.9 trillion hedge fund industry since the financial crisis.

London-based Nevsky Capital closed its doors, citing fewer money-making opportunities because of the emergence of computer-driven strategies and index funds. Tudor Investment Corp. dismissed about 15 percent of its workforce in a shakeup in August. And Brevan Howard Asset Management plans to stop charging existing clients management fees on any new investments they make in two of its hedge funds, according to a person with knowledge of the matter."

In yet another Bloomberg article:

"About 530 funds were liquidated in the first half, on pace for the most shutdowns since 2008."

Bruce Berkowitz, one of the most successful managers in his field and the CIO of Fairholme Capital, is down from $20 billion to $2 billion in a decade! Across the spectrum actively managed mutual funds are down a stunning 79% from 10 years ago.

What's Happening?

Where has the money moved to? One word: passive.

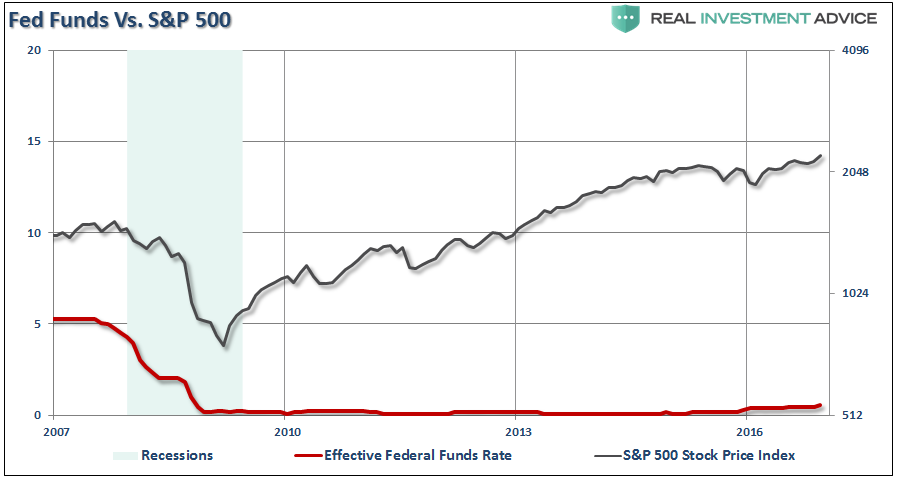

Index funds have much lower fees than active funds and so I can see the appeal. And besides, hedge funds as a group haven't outperformed the US stock market since 2008.

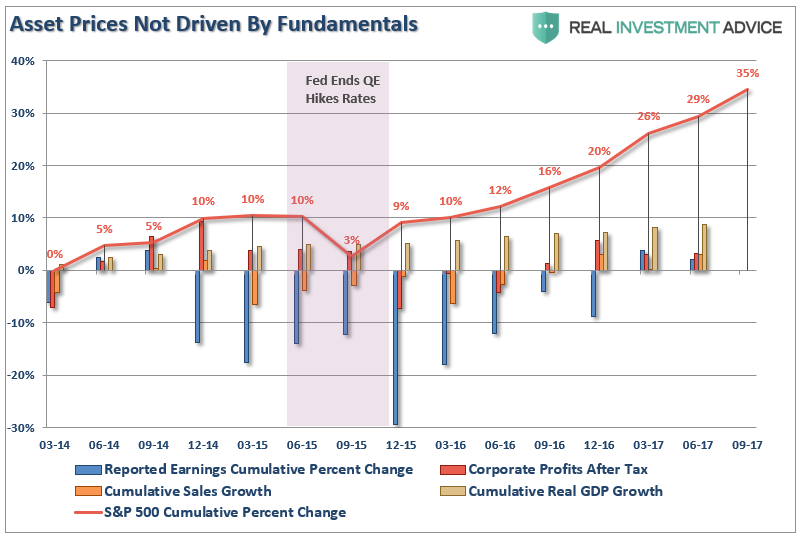

The thing is since 2008 the Fed and global central banks have owned the market. It's no wonder that some of the most talented money managers on this ball of dirt have underperformed the market.

--------------------------------------

--------------------------------------

The question is, is the market right?

Well, the market is always the final arbiter and we have to acknowledge this but in a word, no!

There are two main reasons for that:

Reason 1

Return is only one part of the equation. Risk is its ever present bedfellow. A bedfellow that precious few retail investors understand until they receive a punch to the gut.

Asset managers have a duty to protect capital. This means avoiding risk. So what if an index ETF is beating a fund? How many investors are asking the question why? Clearly not many.

Let me ask you a question. What was widely considered the most stable consistent and safe asset class in 2006?

You're looking at the iShares US Real Estate ETF (IYR). It was THE worst place to be in the coming years.

From a high of 92.5 to 22.21 in a little over 12 months it provided passive index investors what is commonly referred to as a wipeout. But you can't get angry at it. It's just a dumb index doing what it's meant to do.

Now I'm trying to think of just one of my friends or colleagues who was long US real estate in 2006 and 2007 and I can't think of one. Most, including myself, never profited from the collapse but then again we didn't get wiped out either. Did my hedge fund buddies get ridiculed in 2006 for not being long real estate? Of course. But if something doesn't make any sense it pays to stay away.

If you've got a good money manager (and there are some awesome ones out there), then you're paying them for risk adjusted returns.

Reason 2:

Money managers face a tough choice (and it's a choice you as a private investor don't have to worry about): they have to report their quarterly numbers. And if those numbers don't beat the benchmark, they face redemptions.

In today's fast moving world investors' time horizons have narrowed. Like 10-year old Johnny Snot Nose, yet to develop the skills of patience, they want results and they want them now.

This dynamic has forced many money managers to take risks which they really shouldn't be taking, stepping further down the risk curve in order to at least match the benchmark. It's understandable but also daft.

What do you do when the overall indexes are beating you but you see the inherent dangers in the market and refuse to participate, preferring to protect your capital, going to cash, and avoiding overpriced assets?

Well, now we're finding out as investors shun even the best active money managers in favour of "passive investing".

A Bubble Forming

I recently had a conversation with a part-time investor who is managing his money and trying to do it himself. He was buying ETFs because of the low fees, and since they provide him exposure to pretty much any asset class he felt they made sense. All good, except it was a mess when we began to dig deeper.

He'd been buying leveraged ETFs, specifically NUGT which is the 3x leveraged gold shares ETF. I warned about these last week when suggesting to never invest in these horrible things. He bought a healthy chunk in May of 2016 and since GDX (the gold miners index) is essentially flat from the time of his purchase he couldn't understand why he had lost money.

The second thing he'd been doing was he'd bought a half dozen bond ETFs for "safety". When we discussed it he felt that because he owned the big five he was diversified. Now buying sovereign bonds at the tail end of the debt super cycle impresses me as insane and you're not even compensated for the risk!

The other thing he'd been doing, as a hedge against potential market volatility, was to buy a couple of low volatility ETFs. Oy vey!

In short, his portfolio was sporting so much risk it made my head spin.

In the last 5 years over $50 billion has flowed into low volatility ETFs, distorting the stocks they comprise.

Mark Yusko, the founder and CIO of Morgan Creek Capital recently exposed the insanity of what's going on here (and it's also something Chris Mayer and I discussed recently in a podcast).

The assets which are included in many of the ETFs have been heavily skewed by dumb money coming in. Yusko pointed out Exxon Mobil (XOM) which historically has a P/E of 12 but now trades at 35x earnings. Why? Because it's part of an ETF that is on the flip side of all those liquidating hedge funds. Dumb money.

Spectacular!

I can't wait to see this one play itself out. It's going to be more fun than watching Trump and Hillary in a cage fight, which I dare say would be the highest grossing reality TV in history and the one and only reality TV show I'd actually watch.

What Next?

Less money men is a good thing. And though many (like those mentioned above) are being thrown out with the bathwater, I don't see this as being much more than yet another consequence of an extended period of gross mispricing of assets by our monetary overlords.

Howard Marks famously said that the cure for high prices is high prices, and the cure for low prices is low prices.

The hedge fund industry has over the years attracted billions of capital and whenever money flows into a sector we bipeds follow it. Many of those who came to managing money probably should never have been doing so but instead gone into growing marijuana, or making Yorkshire puddings, or farming chickens. Whatever, they shouldn't have been managing money. Now many of them are going to do just that. I look forward to a bubble in Yorkshire puddings.

Passive money is a ludicrous concept. Money is not passive. Your attitude to it may be but it is and always will be dynamic. And so sticking money blindly into index funds and ETFs is almost as daft as it is giving it to your government. Almost!

John Hussman, CIO of Hussman Funds put it succinctly:

"Passive returns look glorious in the rear-view mirror precisely because Fed-induced yield-seeking speculation has driven nearly every asset class to rich or obscene valuations in recent years.

But investors should understand that risky securities do not, over time, persist without risk premiums. Indeed, neither aggressive Fed easing nor low interest rates has historically supported stocks during periods when, for whatever reason, investor preferences shift toward risk-aversion.

This lesson should have been drawn from the 2000-2002 and 2007-2009 collapses. The same lesson is likely to be taught again shortly, as we infer increasing risk-aversion among investors based on deteriorating uniformity and increasing dispersion across market internals. The immediacy of our concerns would ease in response to a material improvement in those internals."

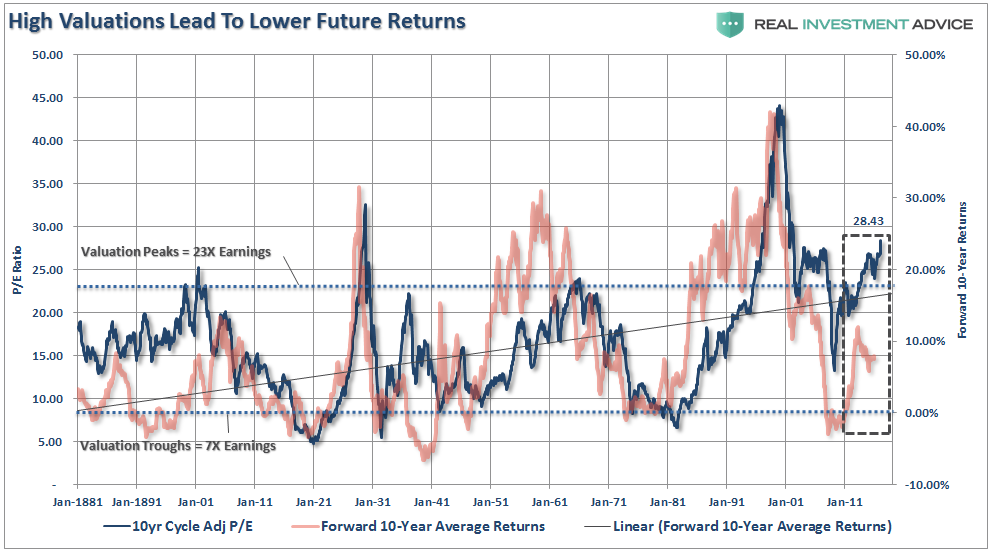

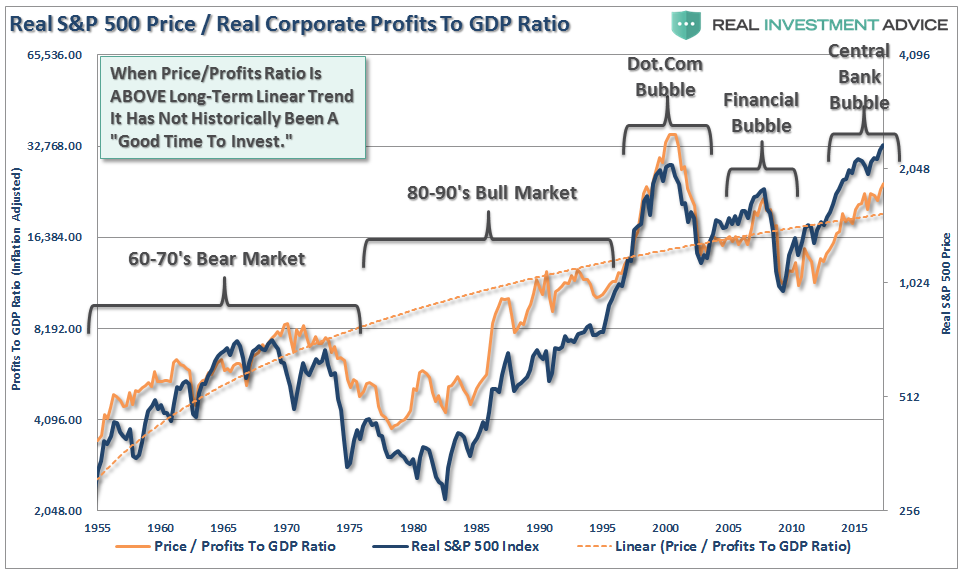

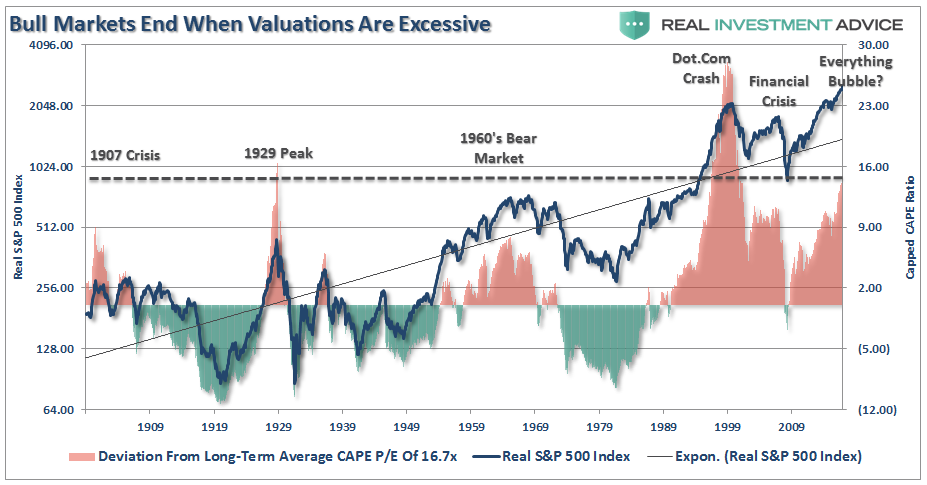

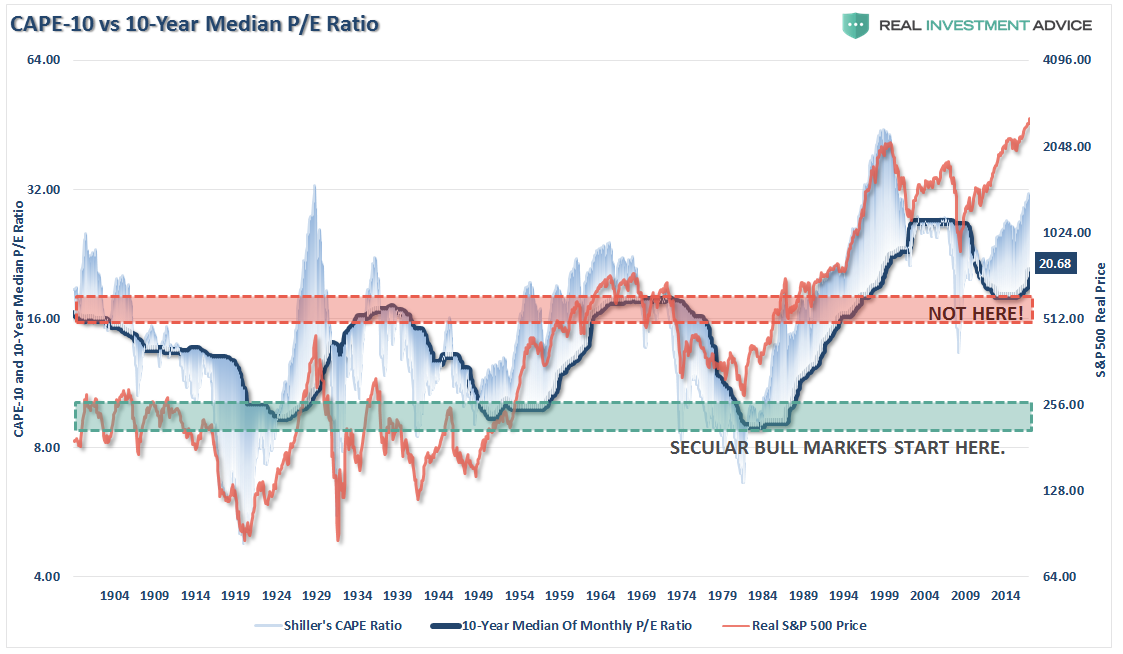

I fear we're about to find out how smart "smart beta" really is. When the inevitable happens and Bob and Mabel, together with their millennial grandkids, Peach and Cloud, lose their shirts there'll be no-one there to explain to them, "sorry, snowflake but did you realise that over half of the index you bought was sporting P/E and P/B ratios that have only existed a couple of times before?"

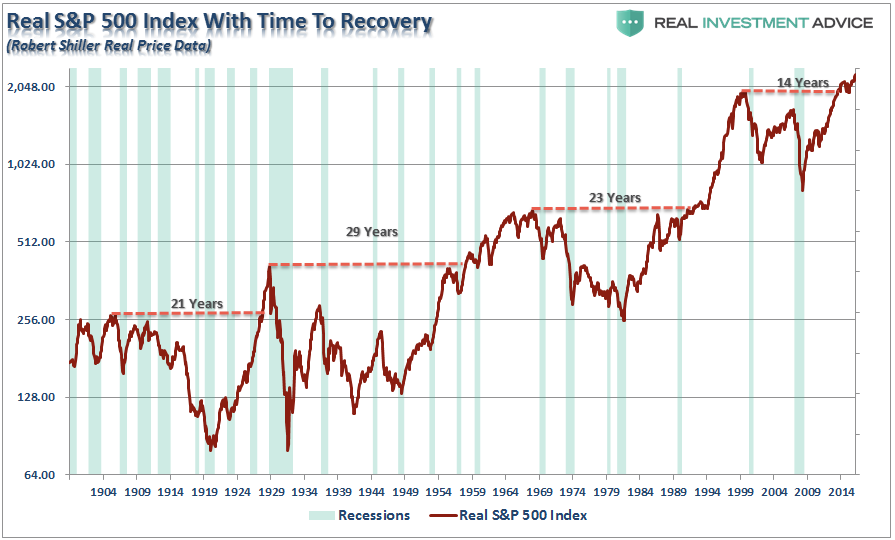

Remember, the 1929 crash took 30 years on an inflation adjusted basis to get back to breakeven. Passively investing in indexes at what looks like the eve of a systemic market shift may well prove the value in active investing.

Question

Cast your vote/leave your comment here and also see what others think

Know anyone that might enjoy this? Please share this with them.

Investing and protecting our capital in a world which is enjoying the most severe distortions of any period in mans recorded history means that a different approach is required. And traditional portfolio management fails miserably to accomplish this.

And so our goal here is simple: protecting the majority of our wealth from the inevitable consequences of absurdity, while finding the most asymmetric investment opportunities for our capital. Ironically, such opportunities are a result of the actions which have landed the world in such trouble to begin with.

- Chris

"An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative."— Benjamin Graham

--------------------------------------

Liked this article? Don't miss our future missives and podcasts, and

get access to free subscriber-only content here.

--------------------------------------