Just when traders thought that the biggest and most violent 3-day short squeeze in 7 years was about to end...

![]()

... a squeeze that has resulted in 3 consecutive 1%+ sessions for the S&P for the first time since October 2011, overnight we got one of the Fed's biggest faux-hakws, St. Louis Fed's Jim Bullard, who said that it would be "unwise" to continue hiking rates at this moment, and hinted that "if needed", the most natural option for the Fed going forward would be to do further Q.E.

At the time the algos ignored his comment, but once Europe opened, the local trading disks hit the buy button, pushing S&P futures from just above 1915 to 1931 where they were trading last.

It wasn't just Bullard: yesterday's Fed minutes were likewise as cautious, if not outright dour, about the future of the Fed's rate hike which was great news for markets as it means the rate hike cycle has been put on indefinite hiatus. "The Fed minutes show that it does look like they’re gearing up for a slower rate hike path, which is good” for risk assets, said Nader Naeimi, Sydney-based head of dynamic markets at AMP Capital Investors Ltd. "I think this rally has further to go, with the conditions set for the rebound to continue for a little while. Pessimism had got to extreme levels."

Actually, as we showed yesterday, what is really happening is one of the most violent unwinds of market neutral quant funds, who finds themselves forced to chase long higher as shorts continue to rip.

![]()

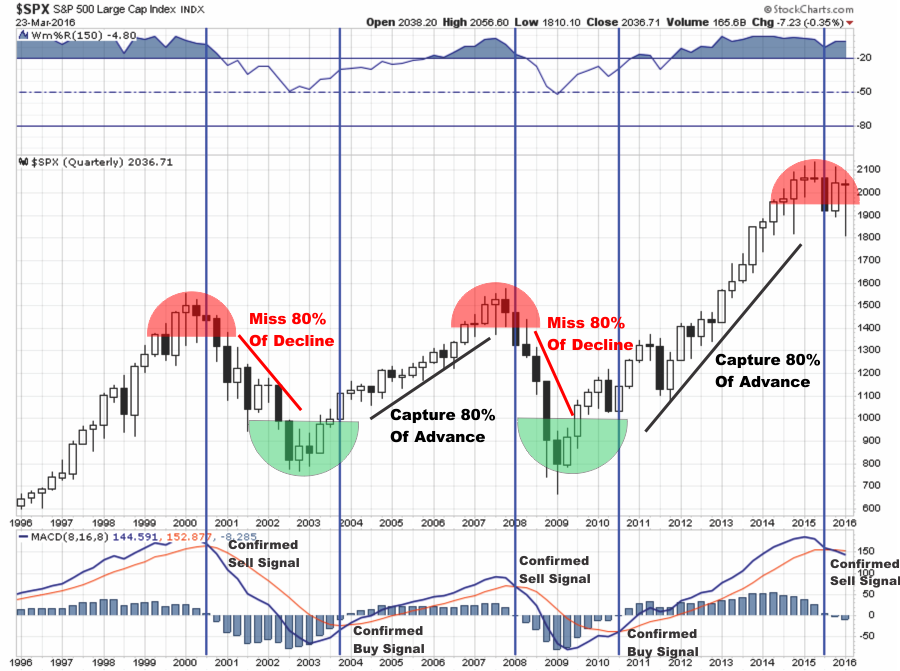

This could easily continue until the S&P rises back over 2000 only this time on forward earnings that are about 10% lower than the last time the market was in such perilous territory.

It wasn't all just a marketwide squeeze: food-related companies and miners weighed on Europe’s equity benchmark while Treasuries advanced, while the yen also climbed. Elsewhere, Emerging markets rose to a six-week high, while the Mexican peso gained a second day after lawmakers took unprecedented steps to protect the currency. Crude extended gains with Iran backing an output freeze by key energy-producing nations.

As Bloomberg writes, "while global stocks are rising for a fifth day, fueled by oil’s rally coupled with the Federal Reserve’s acknowledgment of market gyrations, the pace of gains slowed on Thursday." That sentence was written before the momentum algos were activated today: at the current rate futures are spiking we may see the first 4-day consecutive 1%+ daily streak in the S&P500 in over 4 years.

The cherry on top was the OECD cutting its global growth forecasts, saying the economies of Brazil, Germany and the U.S. are slowing and warning that some emerging markets are at risk of exchange-rate volatility. Global gross domestic product will expand 3.0 percent in 2016, the same pace as in 2015 and 0.3 percentage point less than predicted in November, the Organization for Economic Cooperation and Development said Thursday in a report.

And now that rate hikes are increasingly off the table, bad news is one again great news. After all it means more central planner medling, and long-only algos love that.

Market Wrap

- S&P 500 futures up 0.5% to 1932

- Stoxx 600 up 1% to 332

- FTSE 100 down 0.4% to 6009

- DAX up 1% to 9468

- German 10Yr yield down 2bps to 0.25%

- Italian 10Yr yield down 6bps to 1.55%

- Spanish 10Yr yield down 5bps to 1.69%

- S&P GSCI Index up 0.7% to 302.4

- MSCI Asia Pacific up 2.2% to 120

- US 10-yr yield down 1bp to 1.81%

- Dollar Index up 0.02% to 96.81

- WTI Crude futures up 2.6% to $31.45

- Brent Futures up 1.7% to $35.09

- Gold spot down 0.3% to $1,205

- Silver spot down 0.3% to $15.23

Global Headline News Summary

- Starboard Said to Take Initial Steps for Proxy Battle With Yahoo: Adviser has been calling shareholders, people familiar say

- PBOC to Conduct Open-Market Operations Every Working Day: Seeks to improve effectiveness of operations

- Bullard Calls Raising Rates Unwise as Inflation Falls Short: Asset-price bubbles aren’t a worry amid turmoil, he adds

- Oil Extends Gain as Iran Backs Output Freeze Without Vowing Cuts: Saudi-Russia pact contingent on other major producers joining

- Ingram Micro to Be Bought by Tianjin Tianhai for $6b: U.S. networking supplier to become part of China’s HNA Group

- Credit Suisse Americas ‘One Bank’ Head Leaving Amid U.S. Retreat: Lender retreating from managing money for U.S. clients

- Wells Fargo Said Near Deal to Lease City of London Offices: 225,000 square-foot building scheduled for completion in 2017

- Gasoline Is Trading as If U.S. Nearing Recession, Goldman Says: Contracts for summer delivery are priced less than $20 a barrel higher than crude oil

- Apple Gains Silicon Valley’s Backing in Fight Against Government: Google’s Pichai says U.S. order may set ‘troubling precedent’

- Apple Joins With China’s UnionPay to Introduce Mobile Payments: Clients of 19 Chinese lenders can shop with Apple Pay

- Swiss Watch Exports Drop as Slowing Economies Curb Demand: Hong Kong, U.S. and China drag down global watch shipments

- Obama Said to Plan Cuba Visit in March 55 Years After Ties Cut: Opponents of easing relations fault president over trip

- Chevron Indonesia Plans to Cut at Least 1,200 Jobs, Kontan Reports: Cites Amien Sunaryadi, head of upstream oil and gas regulator, known as SKK Miga

Looking at regional markets, we start in Asia where equity markets traded higher across the board, tracking similar price action from Wall St, as gains in crude and FOMC minutes supported risk-appetite. Nikkei 225 (+2.3%) and ASX 200 (+1.9%) was led higher by the energy sector, after oil rallied around 8% yesterday on optimism regarding an output freeze, coupled with an API Inventory drawdown. Shanghai Comp (-0.2%) was mildly positive for a bulk of the session before paring gains heading lower into the close, after the PBoC upped its liquidity injections with price data also more encouraging after CPI printed a 5-month high, while casino gains added to the energy-led risk sentiment in Hong Kong. 10yr JGBs traded higher as yields continued to decline in the aftermath of the BoJ's negative rate policy with several domestic banks adjusting rates in reaction, although JGBs then reversed some gains after a weaker than prior 5- yr auction.

Top Asian News

- China Said to Guide Rates Lower Without Broader Policy Cuts: Offers to reduce medium-term borrowing cost it charges lenders in 2nd such move this year

- China’s Consumer Prices Climb in January as Food Costs Rise: Food prices rose 4.1% ahead of week-long Lunar New Year holiday, most since May 2014

- Goldman Sachs Top Analyst Says Don’t Panic as China Growth Slows: Most accurate forecaster on nation’s economy projects 6.4% growth this year

- Nomura Sees Yen Falling More Than 10% on BOJ Negative Rates: No intervention seen until dollar falls below 105 yen, Yunosuke Ikeda says

- Australian Unemployment Spikes to 6% as Full-Time Jobs Slump: Nation’s unemployment rate unexpectedly rises to highest since September 2015

- Japan’s Exports Drop Most Since 2009 as Sales to China Fall: Imports also decline, leaving a trade deficit slightly narrower than median forecast

European equities have kicked off the session in modest positive territory today (Euro Stoxx +0.3%), continuing on from the gains seen yesterday. Looking across the indices, FTSE (-0.6%) is among the worst performers after 6 Co.'s in the index went ex-div and knocked off 24 points from the index. Separately, the SMI (-0.5%) also underperforms this morning, weighed on by Nestle (-3.4%) who are among the worst performers on the continent. Elsewhere, Bunds remain bid this morning, all be it off their best level, underpinned by somewhat cautious FOMC minutes yesterday, with supply from Spain and France yet to have a meaningful impact on the price action.

Top European News

- Nestle Sees Sales Slowdown Extending Into ‘16 on Price Pressure: CEO says dividends, M&A outweigh buybacks for uses of cash

- Vodafone to Raise About $4.1 Billion Selling Convertible Bonds: Bonds to carry coupons of 1.2%-1.5%, 1.7%-2%

- Anglo Said to Work With Bank of America on More Coal-Mine Sales: Firm advising on sale of Moranbah, Grosvenor coal assets

- BMW Buoyed U.S. Sales Numbers by Paying Dealers to Buy Loaners: Other carmakers use similar strategy but not as aggressively

- Air France-KLM Gains on First Annual Operating Profit Since 2010: Reduction of 22% in fuel costs helps end run of losses

In FX, it has been a relatively quiet morning, with limited response to the FOMC minutes released late Wednesday. Few were expecting anything ground-breaking after last week's House/Senate testimony, with the wait-and-see mode underlined, so it was anaemic reaction from the USD pairs. Much of the same this morning, with USD/JPY back under 114.00. No panic from the earlier test on the mid 113.00's, but stock market gains have faded a little, though Oil prices remain on the front foot. CAD still well placed for further upside, though the spot rate is still holding off the early Feb lows. MXN took out 18.0000 yesterday, but is back above the figure today. GBP trade cautious with UK PM Cameron in Brussels today and tomorrow, but we have seen some adjustment to the upside a Cable tentatively reclaims 1.4300. It is all pretty tight elsewhere, with EUR/USD still holding off 1.1100 and AUD holding the mid .7100's despite a disappointing jobs report overnight. The Australian dollar declined at least 0.3 percent against all of its 16 major peers after a disappointing jobs report fueled investor doubts about whether the central bank is done cutting interest rates.

In Commodities, West Texas Intermediate crude climbed 2.5 percent to $31.41 a barrel after rallying 5.6 percent last session. U.S. inventories declined by 3.26 million barrels last week, the industry-funded American Petroleum Institute was said to report Wednesday. Oil’s 49 percent slump from a peak reached in June has shaken some crude-dependent economies, with S&P cutting the credit ratings of Saudi Arabia, Oman, Bahrain and Kazakhstan on Wednesday. Key oil producer Venezuela announced a currency devaluation, with the official exchange rate reduced by 37 percent, President Nicolas Maduro said on state TV. The Latin American country also raised gasoline prices for the first time since 1996 as it struggles to avoid defaulting on foreign debt. Copper in London slid 0.6 percent, while gold slipped 0.3 percent to $1,204.80 an ounce in the spot market after jumping 0.7 percent last session.

On today's US event calendar there will be some attention paid to the latest initial jobless claims number following the prior week’s strong data and also given that this will cover the survey period for the February employment report. Also due out is the Philly Fed business outlook for this month where a modest improvement is expected, albeit to a still lowly -3.0 (from -3.5). Later on we’ll get the index of leading economic indicators where a second consecutive negative reading is forecast (-0.2% mom). Earnings wise we’ll hear from 20 S&P 500 companies including Wal-Mart.

Bulletin Headline Summary

- In what has been a relatively tame session so far, EU bourses have extended on yesterday's gains amid outperformance in the Utilities sector.

- Asian equities followed the lead from Wall Street to trade higher, while Chinese CPI printed a 5-month high (albeit below expectations)

- Looking ahead, ECB minutes, US Philly Fed Bus. Outlook and weekly jobs data and comments from Fed's Williams.

- Treasury yields little changed in overnight trading as global equity markets mostly higher, oil rallies and gold sells off as risk sentiment improves.

- David Cameron heads to Brussels seeking to finish off months of negotiations on new European Union membership terms with a deal that he can put to the British people

- Cameron hopes to win concessions during the two-day summit that will pave the way for a referendum to be held in Britain as soon as June, in which voters will decide whether or not the U.K. should remain in the EU

- The final draft of the proposed deal has been leaked, according to the Financial Times

- The OECD cut its global growth forecasts, saying the economies of Brazil, Germany and the U.S. are slowing and warning that some emerging markets are at risk of exchange- rate volatility

- China’s central bank drained the most funds from the financial system in two years, mopping up excess cash from the financial system after flooding lenders with funds in the run-up to last week’s Lunar New Year holiday

- PBOC said it will start conducting open-market operations every business day, strengthening its influence on interest rates

- Oil extended gains above $31 a barrel in New York after industry data showed a decline in U.S. crude inventories, while Iran cautiously supported a proposal by Saudi Arabia and Russia to freeze production at near-record levels

- Iran’s qualified backing of an accord led by Saudi Arabia and Russia to cap output sowed doubts that the agreement can succeed in tempering a record global surplus

- Turkey’s prime minister blamed two Kurdish groups for a bombing in the capital that killed 28 people, ratcheting up tensions with the U.S., which has backed one of them as a major ally in the fight against Islamic State

- $8.1b IG corporates priced yesterday (YTD volume $213.35b) and $500m HY priced yesterday (YTD volume $10.125b)

- Sovereign 10Y bond yields mostly lower led by Greece (-25bp) and Portugal (-18bp); European, Asian markets mostly higher; U.S. equity-index futures higher. Crude oil rallies, copper and gold drop

US Event Calendar

- 8:30am: Philadelphia Fed Business Outlook, Feb., est. -3 (prior -3.5)

- 8:30am: Initial Jobless Claims, Feb. 13, est. 275k (prior 269k)

- Continuing Claims, Feb. 6, est. 2.250m (prior 2.239m)

- 9:45am: Bloomberg Economic Expectations, Feb. (prior 47)

- Bloomberg Consumer Comfort, Feb. 14 (prior 44.5)

- 10:00am: Leading Index, Jan., est. -0.2% (prior -0.2%)

- 1:00pm: U.S. to sell $7b 30Y TIPS

- 3:30pm: Fed’s Williams speaks in Los Angeles

DB's Jim Reid concludes the overnight wrap

The S&P 500 (+1.65%) completed its first 3-day gain of the year yesterday, WTI Oil (+5.58%) is now 20% off the lows and at levels first breeched on the downside on January 11th. So we've had nearly 6 weeks of range trading rather than the relentless falls of the prior period. Also iTraxx financial senior (-9bps) and sub (-31bps) are 26bps and 65bps off their wides from last week.

US data continues to also hold up considering the recent market stress. Various economic surprise indices are pointing up for the first time in many weeks even if there are still some misses (yesterday’s housing starts an example). Interestingly industrial production (+0.9% mom vs. +0.4% expected) picked up strongly yesterday albeit with downward revisions to the previous month. As can be seen from the graph in today's pdf, despite yesterday's mom pick-up, industrial production (on a yoy basis) has never been this negative without it signalling a recession. Indeed IP has been a very reliable indicator of upcoming recessions. However we've been slightly dubious of this link in this cycle because it's been so obvious that the manufacturing sector has never before been so decoupled from the much larger service sector so it could be a false signal this time. Yesterday's rebound confuses this further, especially as we're still negative yoy. As a reminder we are fully paid up secular stagnation fan club members but we don't think the US is going into recession... yet!!!

Before we recap the highlights from yesterday, an update on the latest in China where the January inflation numbers have been released this morning. CPI was reported as rising +0.5% mom last month having been driven by a surge in food prices with non-food prices relatively stable. It’s worth warning that food prices tend to be subject to bouts of volatility and seasonality though. However, as a result that’s seen the YoY rate lift two-tenths to +1.8% although slightly less than the +1.9% expected by the market. That said, the data is trending in the right direction after CPI dipped as low at +1.3% in October and +0.8% twelve months ago. There is better news to come out of the January PPI print too which has risen six-tenths to -5.3% yoy (vs. -5.6% expected). That does however mark 47 consecutive months of factory gate deflation.

Looking at the market reaction, there’s been some modest gains for bourses in China with the Shanghai Comp and Shenzhen +0.52% and +0.56% respectively. Bourses elsewhere are trading with a decent tone meanwhile and seemingly following the lead from the US last night. The Nikkei (+3.02%) has gained despite some soft export data overnight (-12.9% vs. -10.9% expected) while the Hang Seng (+2.32%), ASX (+2.25%) and Kospi (+1.09%) are also up strongly. Credit markets are materially tighter while Oil is up another 2% this morning. That’s also keeping US equity futures in the green.

Yesterday saw the release of the FOMC minutes from the January policy meeting. While still a big focus, Yellen’s recent comments at her Semi-Annual Testimony meant a lot of the text was already pre-flagged. Overall the message pointed towards one of the Fed still being in a wait and see mode, keeping options open but with clear uncertainty around the outlook. A lot of the focus was on the factors driving the turmoil in markets in January with the text showing that ‘while acknowledging the possible adverse effects of the tightening of financial conditions that had occurred, most policymakers thought that the extent to which tighter conditions would persist and what that might imply for the outlook were unclear, and therefore judged that it was premature to alter appreciably their assessment of the medium-term outlook’. That being said, there was however the mention that ‘uncertainty had increased’ and so ‘many saw that these developments as increasing the downside risks to the outlook’.

It was also highlighted that ‘a number of participants indicated that, in light of recent developments, they viewed the outlook for inflation as somewhat more uncertain or saw the risks as being to the downside’. Unsurprisingly China was also highlighted as a concern amongst policymakers as well as the broader effects of a greater than expected slowdown in other emerging markets. A telling stat was that the word ‘uncertainty’ or ‘uncertain’ was mentioned 14 times compared to seven times in the December minutes.

Meanwhile, Boston Fed President Rosengren provided his updated view yesterday. His comments echoed a lot of what was said in the minutes, saying specifically that ‘recent global events may make it less likely that the 2% inflation target will be achieved as quickly as had been projected in forecasts’. As a result, Rosengren said that ‘if inflation is slower to return to target, monetary policy normalization should be unhurried’. St Louis Fed President Bullard followed this up with comments late last night saying that ‘I regard it as unwise to continue a normalization strategy in an environment of declining market-based inflation expectations’.

All said and done the combination of yesterday’s minutes and the economic data did see the probability of a Fed rate hike by the end of this year nudge up to 41% from 34% on Tuesday. 10y Treasury yields closed up just shy of 5bps at 1.820% although were lower post the minutes.

The other main focus yesterday was again on Oil where along for gain for WTI, Brent rallied +7.21% to $34.50/bbl. Attention was centered on the Iran meeting where we had confirmation (WSJ) from the Iranian Oil Minister that they would support a plan from Saudi Arabia and Russia to curb production at January levels. That being said it still feels like there is a lot of noise around this with Iran not actually committing to anything specifically and with little obvious signal that they will be taking part in the production freeze.

For now though the fact that talks are happening appears to be fueling the better sentiment with the moves for Oil enough to support a strong risk-on day yesterday. Along with the gains across the pond, European bourses finished with big moves of their own with the Stoxx 600 closing +2.62% which means it has now finished with a daily gain of at least 2.6% in three of the last four trading days.

Meanwhile in terms of the rest of yesterday’s economic data, along with yesterday’s strong IP report in the US, manufacturing production was also up a better than expected +0.5% mom in January (vs. +0.2% expected) which was actually the most since July, while capacity utilization rose six-tenths to 77.1% (vs. 76.7% expected) although it’s worth highlighting that we did see downward revisions to December reports for this, MP and IP. Elsewhere building permits declined by less than expected last month (-0.2% mom vs. -0.3% expected) to go with the steep fall for housing starts (-3.8% mom). January US PPI was better than expected at the headline (+0.1% mom vs. -0.2% expected) although the YoY rate is still in deflationary territory (at -0.2%). That said the core was up a better than expected +0.4% mom last month (vs. +0.2% expected), lifting the YoY rate to +0.6%.

Meanwhile in the UK the December ILO unemployment rate stayed unchanged at 5.1% (vs. 5.0% expected), although earnings data was a little better than expected with average weekly earnings ex bonus up +2.0% in the three months to December (vs. +1.8% expected).

Taking a look at the day ahead now, the early data out of Europe this morning will come in France where the final revisions to January CPI are expected (no change expected at -1.0% mom). Away from that and due out just after midday will be ECB minutes from the January meeting which will be worth keeping an eye on. Over in the US this afternoon there will be some attention paid to the latest initial jobless claims number following the prior week’s strong data and also given that this will cover the survey period for the February employment report. Also due out is the Philly Fed business outlook for this month where a modest improvement is expected, albeit to a still lowly -3.0 (from -3.5). Later on we’ll get the index of leading economic indicators where a second consecutive negative reading is forecast (-0.2% mom). Away from the data the Fed’s Williams is due to speak tonight on his economic outlook at 8.30pm GMT. The Eurogroup’s Dijsselbloem is due to speak this morning at the EU Parliament Panel while the leaders of 28 EU governments are set to begin a two-day summit in Brussels where the Brexit debate and refugee crisis are expected to be hot topics. Earnings wise we’ll hear from 20 S&P 500 companies including Wal-Mart.

Hitesh is the head of AQR's Global Trading Strategies group, running the firm's trading desk and overseeing the group that builds automated trading models and does transaction cost analysis for equities, futures and FX globally. Prior to AQR, he was the global head of liquidity management at Investment Technology Group, where he built its algorithmic trading platform and managed its crossing network, POSIT. He has published several papers on market structure, algorithmic trading, dark pools and transaction cost analysis, and is listed as a co-inventor on three patents. Hitesh earned a B.Eng. in computer science and engineering from JNV University in Jodhpur, India, and an M.B.A. from New York University.

Hitesh is the head of AQR's Global Trading Strategies group, running the firm's trading desk and overseeing the group that builds automated trading models and does transaction cost analysis for equities, futures and FX globally. Prior to AQR, he was the global head of liquidity management at Investment Technology Group, where he built its algorithmic trading platform and managed its crossing network, POSIT. He has published several papers on market structure, algorithmic trading, dark pools and transaction cost analysis, and is listed as a co-inventor on three patents. Hitesh earned a B.Eng. in computer science and engineering from JNV University in Jodhpur, India, and an M.B.A. from New York University.